What Is Cross-Chain MEV?

It may be tempting to assume that value extraction in blockchain systems remains confined to a single network, yet a different behavior has been observed once interoperability layers and cross-chain execution routes are introduced. Execution conditions are no longer isolated, and transaction ordering can be influenced across multiple environments. As a result, maximal extractable value (MEV) has been extended beyond single-chain boundaries into cross-domain systems. This article examines how cross-chain MEV emerges, how it is expressed through arbitrage and bridge mechanisms, and why shared sequencing and solver-based execution have become relevant. A structured breakdown is provided to clarify how value leakage and extraction patterns are formed across decentralized execution environments.

What Is MEV?

MEV, or Maximal Extractable Value (MEV), refers to the value that can be extracted by controlling transaction ordering, inclusion, or exclusion within a block. It was originally observed in single-chain environments such as Ethereum, where validators or searchers could reorder transactions for profit.

Miner Extractable Value

Earlier systems, particularly in proof-of-work environments, framed MEV as Miner Extractable Value, where miners were positioned at the point of block production. Because transaction ordering, inclusion, or exclusion was controlled at the mining stage, value extraction opportunities were primarily associated with block producers. Under these conditions, reordering could be applied directly before final block construction, and extraction was limited to entities with mining rights over a specific block.

Maximal Extractable Value

As consensus systems transitioned toward proof-of-stake and modular sequencing architectures, control over ordering was no longer limited to miners alone. The concept was therefore generalized into Maximal Extractable Value, where any participant influencing transaction ordering, validators, searchers, builders, or automated bots, may extract value. This includes systems where execution is mediated by block builders, rollup sequencers, or MEV-aware routing layers, expanding the scope beyond base-layer block production.

Why MEV Exists?

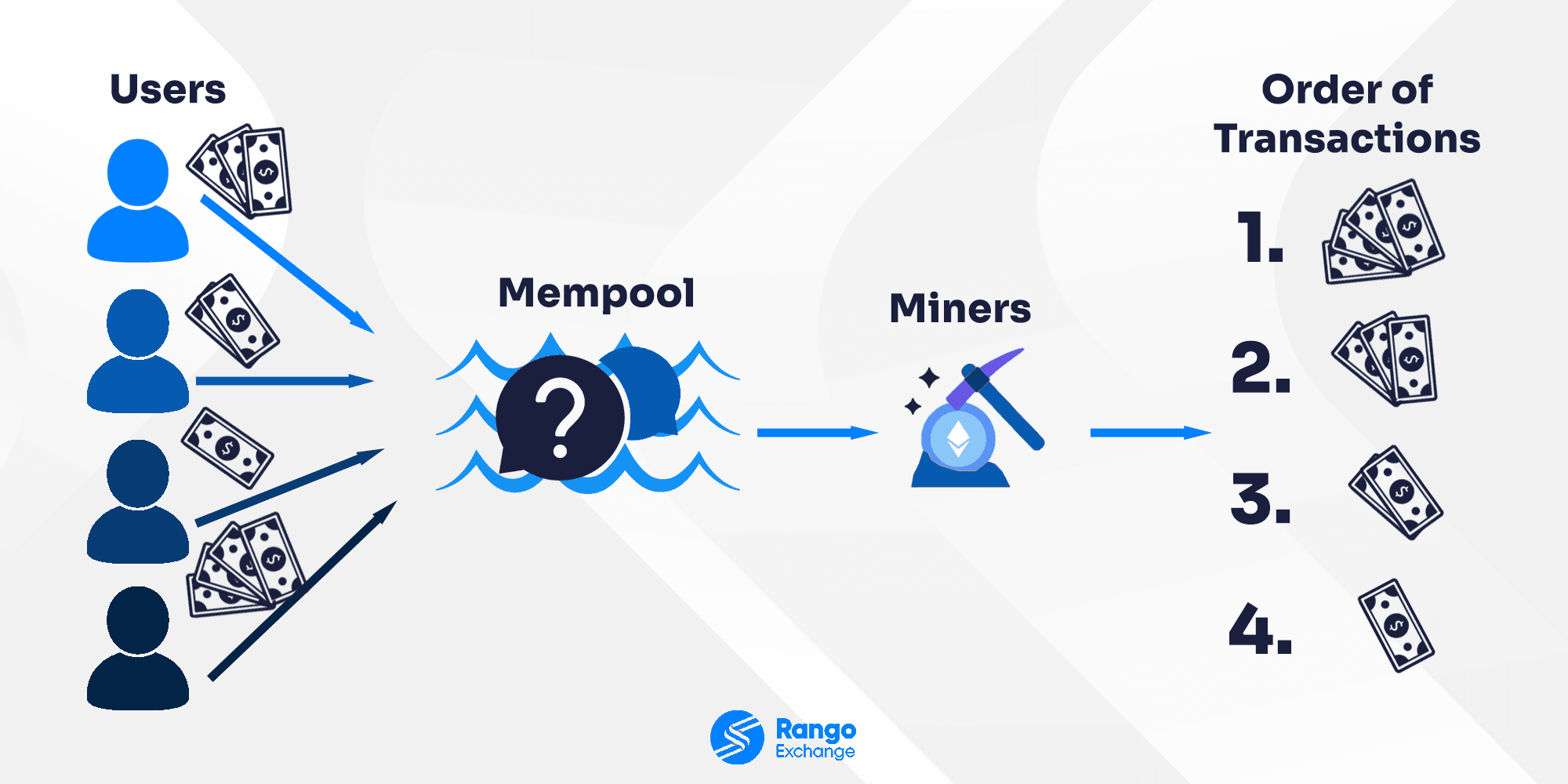

MEV persists due to structural properties of decentralized execution environments. A key factor is the presence of transparent mempools (public transaction queues before confirmation), where pending transactions are visible before inclusion. Additionally, asynchronous propagation of transactions across nodes creates timing differences in what different actors observe. Finally, deterministic execution (same input leads to same output across nodes) ensures that profitable ordering strategies can be reliably reproduced.

Under these combined conditions, pricing inefficiencies frequently emerge in systems such as decentralized exchanges (DEXs) and liquidation markets. When transactions are publicly visible before final confirmation, ordering adjustments can be applied to capture arbitrage spreads or liquidation opportunities before equilibrium is restored.

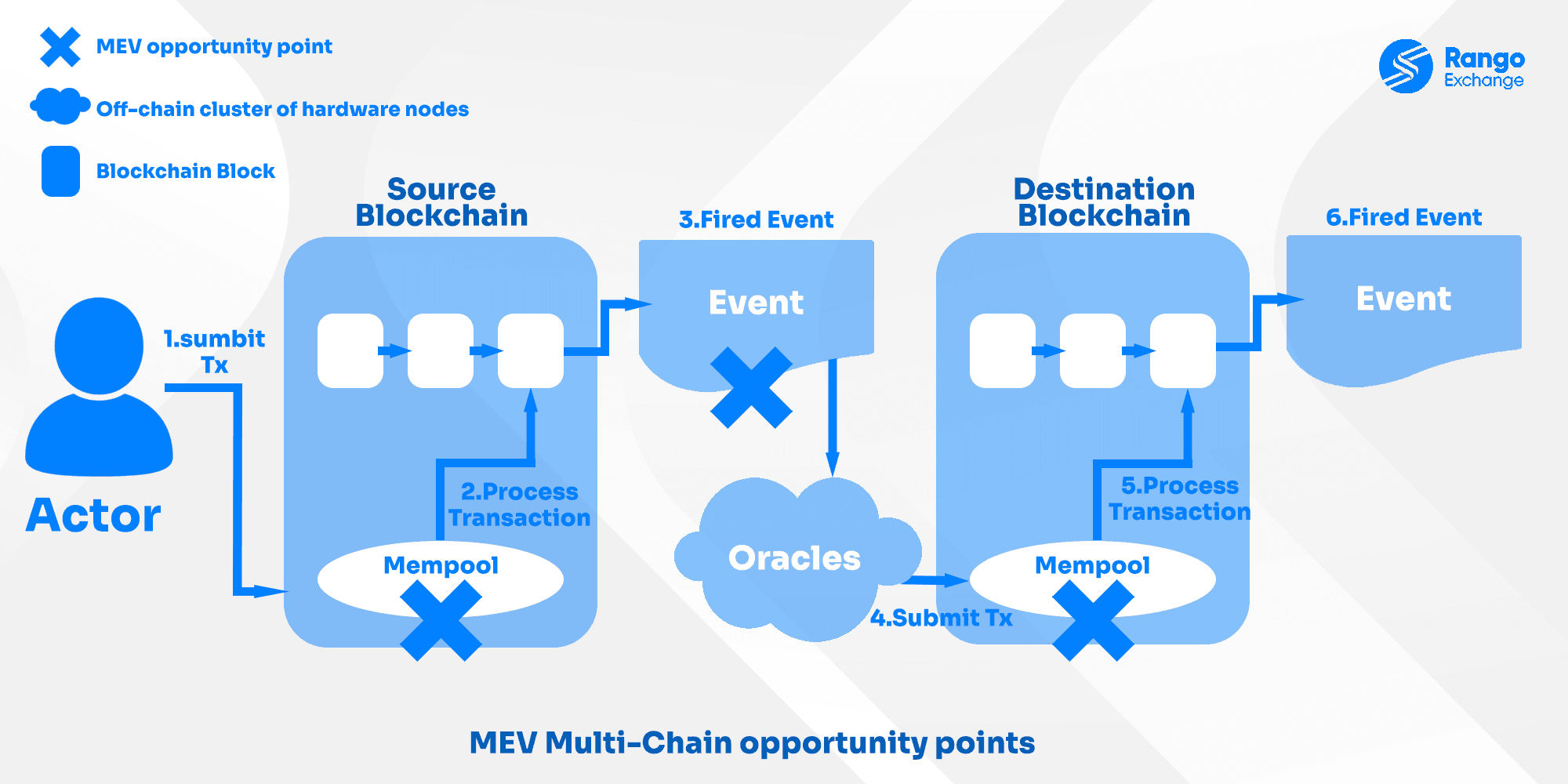

What Is Cross-Chain MEV?

Cross-chain MEV is observed when execution advantages are derived across multiple blockchain networks rather than within a single chain. This typically emerges in environments where bridges, rollups, and interoperability protocols connect liquidity pools and execution layers.

Cross-Chain Arbitrage

Price differences between chains are frequently observed across decentralized exchanges and DEX aggregators (systems that route trades across multiple liquidity sources). When liquidity is fragmented, identical or closely related assets may trade at different prices on separate networks. In such conditions, assets can be swapped on one chain and subsequently bridged to another where pricing is more favorable.

A latency-sensitive arbitrage surface is therefore formed, where profitability is strongly dependent on execution timing. Even small delays in confirmation, routing, or bridge settlement may determine whether the price differential is captured or already corrected by competing actors.

Multi-Chain Execution

Execution in cross-chain environments is typically distributed across heterogeneous systems, including execution layers, bridges, and settlement mechanisms. Each system operates with different finality assumptions and confirmation speeds.

As a result, a temporal gap is often introduced between the confirmation of a transaction on one chain and its effective finality on another. During this interval, state changes may remain partially observed or not yet synchronized across systems, creating conditions where value extraction strategies can emerge. This fragmented execution model increases sensitivity to ordering, routing decisions, and relay timing.

Risks of Moving Assets Across Chains

When assets are transferred across chains, several structural risks are introduced. Bridge delay (time lag between initiation and final settlement) can create temporary exposure where funds are neither fully secured nor fully available. Additionally, inconsistent finality assumptions between chains may lead to ambiguous state interpretation during transition phases.

Message replay vulnerabilities (re-execution of valid messages in unintended contexts) may also arise in poorly isolated systems. Collectively, these conditions expand the observable MEV surface area by introducing timing gaps and state asymmetries, which can be exploited or may unintentionally affect transaction ordering outcomes.

How Cross-Chain Arbitrage Works?

Cross-chain arbitrage is typically driven by price differences, liquidity imbalances, and execution timing. Prices are continuously discovered across decentralized exchanges, yet synchronization delays between chains create temporary mispricings. Liquidity fragmentation ensures that identical assets may trade at different valuations depending on the network. Execution timing becomes critical because bridge finality and block confirmation speeds vary significantly, often ranging from seconds to several minutes depending on the protocol.

A small delay in bridge settlement may allow arbitrageurs or automated solvers to capture spreads before market rebalance. This dynamic is frequently amplified by DEX aggregators, where routing decisions are computed across multiple liquidity sources simultaneously.

MEV in Bridges

Bridge Delays

Bridges introduce asynchronous settlement (non-simultaneous finalization of state between chains), where messages and asset transfers do not resolve instantly across networks. It has been observed that propagation delays between origin and destination chains create short-lived windows in which state consistency is incomplete.

During these intervals, transaction ordering may be effectively “out of sync,” allowing competing actors to observe, react, or submit transactions under different state assumptions. This mismatch can result in exploitable timing gaps where reordering advantages or duplication-based strategies may emerge before final settlement is fully recognized across all systems.

Settlement Exploits

When settlement verification is delayed, intermediate states between initiation and final confirmation may remain economically relevant. In such conditions, speculative execution (acting on partially confirmed or expected state transitions) may be performed based on anticipated final outcomes rather than finalized data. A typical pattern involves liquidity being positioned in advance of final bridge confirmation, where state transitions are inferred before full finality is reached. This can create temporary informational asymmetries between chains, where one side operates on a near-final state while another still reflects pre-settlement conditions. Under these circumstances, execution strategies may be structured around expected settlement rather than confirmed settlement, increasing sensitivity to timing precision.

Liquidity Attacks

Liquidity in cross-chain environments may become temporarily imbalanced during bridging cycles, particularly when large transfers are in transit or not yet fully settled. During these periods, automated routing systems and DEX aggregators may encounter distorted pricing signals. If pricing or reserve ratios diverge across venues, routing logic may be influenced toward suboptimal paths, allowing value extraction from transient inefficiencies. These effects are typically short-lived, but they can be amplified under high volatility or congested bridge conditions, where liquidity redistribution lags behind actual market demand.

Do Cross-Chain Aggregators Prevent MEV?

Cross-chain aggregators are designed to optimize trade execution by routing transactions through the most efficient combination of decentralized exchanges, bridges, and liquidity sources. In some cases, particularly when combined with intent-based execution, batch auctions, or private order flow, they can reduce user exposure to certain forms of MEV such as front-running and sandwich attacks. By allowing multiple solvers to compete for execution, part of the extractable value may be returned to users through better pricing rather than being captured by a single searcher or validator.

However, cross-chain aggregators do not eliminate MEV. The underlying causes of cross-chain MEV, fragmented liquidity, asynchronous settlement, bridge latency, and differing finality models, still exist regardless of the routing mechanism. Aggregators simply choose execution paths within these conditions and may even create new competitive dynamics among solvers seeking the most profitable execution route. As a result, MEV is often redistributed or mitigated rather than prevented. Therefore, cross-chain aggregators should be viewed as tools that improve execution efficiency and can reduce certain MEV risks, but they are not a complete solution for preventing cross-chain MEV.

How Solvers Interact With MEV

Intent Execution

In intent-based systems, users define desired outcomes rather than specifying exact transaction sequences or routing paths. An intent (a declarative expression of desired trade or state change) is broadcast to a solver network, where execution responsibility is delegated to external agents.

Solvers then compute optimal execution routes across multiple chains, liquidity venues, and bridging layers. This may include splitting orders, selecting routes through DEX aggregators, or coordinating cross-chain settlement steps. Because execution paths are not fixed at submission time, the final transaction structure can vary depending on market conditions, liquidity availability, and latency constraints at the moment of resolution.

Solver Competition

When multiple solvers observe the same intent, a competitive environment is formed around execution rights. Each solver may attempt to produce the most efficient or profitable route, balancing speed, gas costs, and liquidity access.

This competition can act as a partial MEV redistribution mechanism. Instead of a single entity capturing ordering advantage, value may be shared or bid away through competition. However, MEV is not fully removed; it is often transformed into a bidding process where execution quality and speed become the primary competitive dimensions.

Order Flow Auctions

In order flow auction systems, user intents or transaction rights are effectively auctioned to solvers. Execution rights are allocated to the highest bidder or most optimal solver based on predefined criteria such as price improvement, execution speed, or settlement guarantees.

This structure shifts MEV capture from passive extraction to explicit pricing of order flow. Value that would otherwise be extracted through ordering manipulation may instead be internalized into auction bids. As a result, MEV becomes more observable and formalized, but it may still persist as it is redistributed between users, solvers, and infrastructure participants.

What Are Shared Sequencers?

Shared Ordering

Shared sequencers introduce a unified ordering layer (a system responsible for deciding transaction sequence before execution) across multiple rollups or connected execution environments. Instead of each chain or rollup independently ordering transactions, a shared sequencing mechanism can coordinate ordering decisions across domains. This reduces fragmentation in transaction sequencing, where previously isolated mempools and independent sequencers could produce inconsistent ordering outcomes. In practice, a more globally consistent view of pending transactions may be maintained, which can reduce divergence in execution ordering between chains.

Cross-Chain Coordination

Cross-chain coordination refers to the alignment of sequencing, message passing, and settlement timing across multiple networks. Timing mismatches, often caused by differences in block times, finality models, and bridge latency, are a primary driver of cross-chain MEV opportunities. When coordination is improved, fewer discrepancies arise between observed and finalized states across chains. This reduces the window in which transactions can be strategically reordered based on inconsistent cross-chain observations. However, perfect synchronization is rarely achieved, and residual latency differences may still preserve limited MEV surfaces.

MEV Reduction

By centralizing ordering logic while preserving decentralized execution, shared sequencing systems aim to reduce observable MEV opportunities without fully eliminating them. The separation of ordering and execution allows systems to control transaction sequencing more predictably, limiting adversarial reordering strategies. However, MEV is typically redistributed rather than removed. It may shift toward sequencer-level auction mechanisms, latency advantages, or cross-domain solver competition. As a result, while apparent arbitrage windows may shrink, underlying value extraction dynamics may still persist in modified forms.

Can Cross-Chain MEV Be Prevented?

Cross-chain MEV cannot be fully prevented, though it can be partially constrained through architectural changes that reduce transaction visibility and ordering manipulability. When private mempools (hidden transaction pools that restrict public pre-confirmation access) are used, pending transactions are no longer broadly observable, which limits opportunities for pre-execution reordering or latency-based exploitation. In parallel, MEV protection mechanisms such as batch auctions or sealed-bid execution systems may be introduced, where transactions are executed in aggregated rounds or with hidden bidding phases, reducing the advantage of real-time ordering competition. In intent-based systems, MEV exposure can be further abstracted by allowing users to specify outcomes rather than execution paths; however, even in such designs, solver competition may reintroduce similar dynamics at the routing and fulfillment layer, where execution rights and optimal paths are still competitively allocated. As a result, MEV is typically reshaped rather than eliminated, shifting between mempool visibility, solver markets, and sequencing infrastructure.

Why Cross-Chain MEV Matters?

Cross-chain MEV directly impacts user execution costs, protocol liquidity efficiency, and overall system fairness. Increased fragmentation leads to higher spreads and unpredictable execution outcomes. In institutional contexts, execution risk is often amplified due to bridge dependencies and latency sensitivity. From a systems perspective, cross-chain MEV indicates that execution environments are no longer isolated. Instead, they behave as interconnected pricing surfaces where latency, liquidity distribution, and routing logic collectively determine extractable value. Consequently, understanding cross-chain MEV has become an important aspect of Web3 security, as the security and efficiency of modern blockchain ecosystems increasingly depend on how value moves across interconnected networks.

Summery

Cross-chain MEV is formed when transaction ordering advantages extend across multiple blockchain networks. It is primarily driven by arbitrage opportunities, bridge delays, and solver-based execution systems. While shared sequencers and private mempools may reduce certain inefficiencies, the underlying condition, fragmented liquidity and asynchronous execution, remains persistent. As a result, MEV is not removed but redistributed across different layers of the execution stack. A careful understanding of cross-chain dependencies is required when interacting with multi-chain systems, especially under high volatility or low-latency conditions.

Resources

Frequently asked questions

Check out most commonly asked questions, addressed based on community needs. Can't find what you are looking for?

Contact us, our friendly support helps!

What is cross-chain MEV in crypto?

Cross-chain MEV (Maximal Extractable Value) refers to profit opportunities created by transaction ordering, timing differences, and liquidity fragmentation across multiple blockchain networks. Unlike traditional MEV, which occurs on a single chain, cross-chain MEV arises when bridges, rollups, and interoperability protocols create temporary inefficiencies that can be exploited through arbitrage, liquidations, or optimized execution strategies.

How does cross-chain arbitrage work?

Cross-chain arbitrage occurs when the same asset is priced differently on separate blockchains. Traders, bots, or solvers purchase the asset on the lower-priced chain and sell it on the higher-priced chain, often using bridges or cross-chain liquidity networks to move assets. Profitability depends on factors such as execution speed, bridge settlement times, transaction fees, and market volatility.

Can cross-chain MEV be fully eliminated?

No. Cross-chain MEV is a structural consequence of fragmented liquidity, asynchronous settlement, and differing finality models across blockchain networks. While it cannot be completely removed, its impact can be reduced through mechanisms such as private mempools, shared sequencers, batch auctions, intent-based execution, and improved cross-chain coordination that limits exploitable timing and ordering advantages.