What is Know Your Customer (KYC) and Why is it Important?

As money becomes more digital, so do the risks. That’s where Know Your Customer (KYC) comes in. Whether it’s fiat or crypto, the challenge today isn’t just moving capital, it’s making sure it’s clean, traceable, and accountable. KYC is a foundational element in preventing illicit activity and establishing legitimacy in finance and crypto ecosystems. Governments and businesses worldwide enforce KYC standards to protect the integrity of their financial systems.

Understanding the concept of Know Your Customer (KYC)

Before exploring its importance, we need to understand what KYC truly entails and how it fits within broader compliance efforts.

Definition and origins of KYC

KYC refers to the process of verifying a customer's identity before or during the time they start doing business with financial institutions. It originated in the early 2000s after the 9/11 attacks, when U.S. regulations like the USA PATRIOT Act mandated stricter controls on financial transactions to combat terrorism and money laundering. KYC forms a critical part of Customer Due Diligence (CDD) procedures, ensuring that institutions know who they’re dealing with. Over time, it has become a global standard, embedded in international anti-money laundering (AML) frameworks.

How KYC fits into the broader compliance framework

KYC is one element within a comprehensive compliance structure that includes:

Together, these ensure institutions not only meet regulatory requirements but also reduce business risks. In decentralized finance (DeFi), platforms now integrate KYC as part of hybrid security models.

Why KYC is important in modern financial systems?

KYC is more than a box to check; it’s a proactive approach to security and operational integrity.

Preventing fraud and financial crimes through KYC

By enforcing identity verification, KYC helps in:

KYC ensures that individuals provide valid IDs, making it difficult for criminals to use fake identities in financial transactions.

By verifying identities and monitoring transactions, KYC helps identify and stop suspicious activities that could involve laundering illicit money.

According to the Financial Action Task Force (FATF), KYC helps track and block funds that might support terrorism by identifying and monitoring high-risk individuals or entities.

Many crypto exchanges and fintech platforms have adopted automated KYC procedures to keep up with fast onboarding while complying with international standards.

Building trust between businesses and customers

Beyond preventing fraud, KYC fosters trust between businesses and their customers. When users go through identity verification:

As a result, KYC doesn't just protect businesses; it also strengthens the overall reputation of platforms, making them more attractive to potential customers who value security and trust.

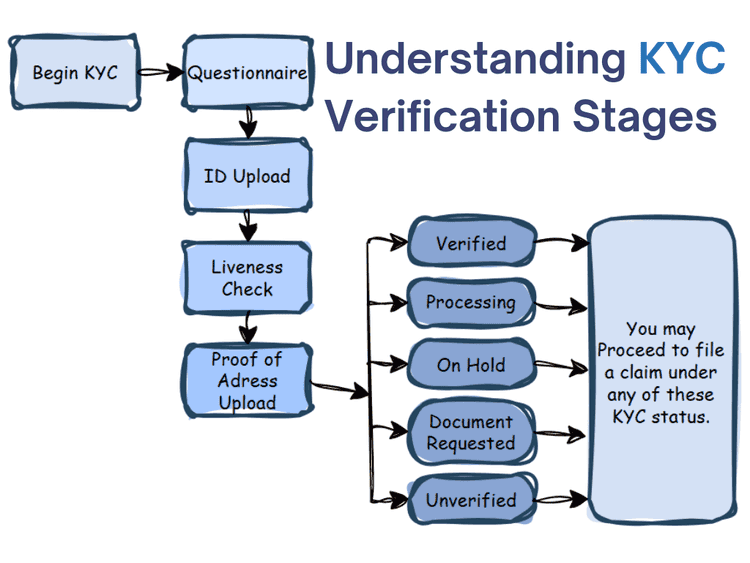

Key components of a KYC process

A typical KYC process isn't one-size-fits-all. However, most systems follow a two-phase structure to ensure thoroughness.

Identity verification and document submission

This is the first step and usually includes:

Institutions cross-check this data with public databases and blacklist registries. The process has now evolved to include AI-driven facial recognition and liveness detection for added security.

Ongoing monitoring and risk assessment

KYC isn’t a one-time event. Businesses must continuously monitor customer behaviour to detect:

Modern platforms employ automated tools to handle risk-based assessments, flag inconsistencies, and generate real-time alerts. This not only ensures regulatory compliance but also guards against emerging threats.

Challenges and advancements in KYC implementation

Despite its benefits, KYC has some friction points, especially in fast-moving, tech-driven sectors like crypto.

Balancing customer privacy with regulatory compliance

One of the main criticisms of KYC is the intrusion into user privacy. People worry about:

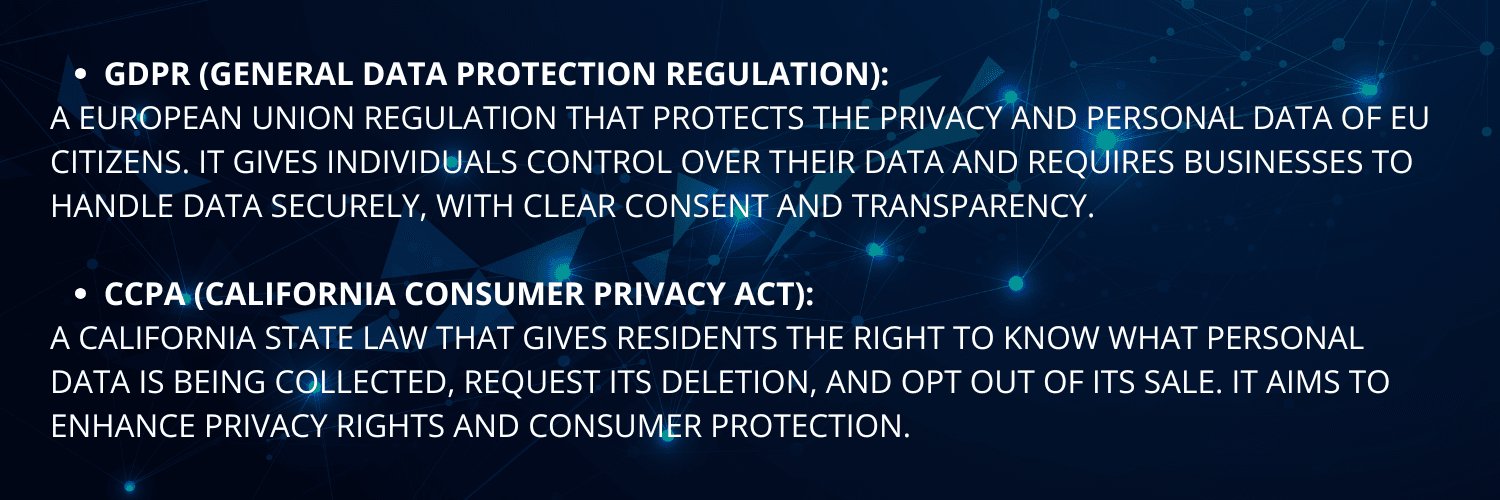

Hence, platforms must follow strict data protection regulations like GDPR and CCPA, ensuring that collected information is securely stored and only used for legitimate purposes.

Leveraging technology for efficient KYC processes

To meet the demands of both compliance and user experience, companies are increasingly turning to RegTech (Regulatory Technology). This includes:

Such solutions drastically reduce KYC processing time and enhance accuracy. According to a report by Deloitte, RegTech adoption has increased by over 60% among financial institutions since 2020.

Conclusion

Know Your Customer (KYC) isn't just about regulation; it's about building safer, more transparent financial ecosystems. From its origins in anti-terror legislation to its modern digital evolution, KYC continues to evolve to meet the demands of today’s economic landscape. As technology continues to expand access to financial services globally, strong and efficient KYC protocols are key to protecting systems, preventing abuse, and fostering trust. Whether you’re a fintech founder, crypto trader, or institutional banker, understanding and implementing proper KYC is no longer optional; it’s essential.

“Privacy is not the opposite of accountability.”

– Andreas M. Antonopoulos, Bitcoin advocate and security expert

Resources

Frequently asked questions

Check out most commonly asked questions, addressed based on community needs. Can't find what you are looking for?

Contact us, our friendly support helps!

What happens if I don't complete KYC on a platform?

Centralized platforms will typically restrict your access to services like trading, withdrawals, or deposits until you verify your identity through KYC. If you prefer to avoid KYC, you may consider using decentralized platforms, which often allow access without identity verification.

Is KYC mandatory for decentralized finance (DeFi)?

While traditionally not required in DeFi, some platforms now incorporate optional or hybrid KYC to comply with evolving regulations and improve safety.

Can KYC data be hacked or misused?

Yes, if platforms don’t follow strong cybersecurity practices. Choose platforms with encryption, two-factor authentication, and a transparent data policy.